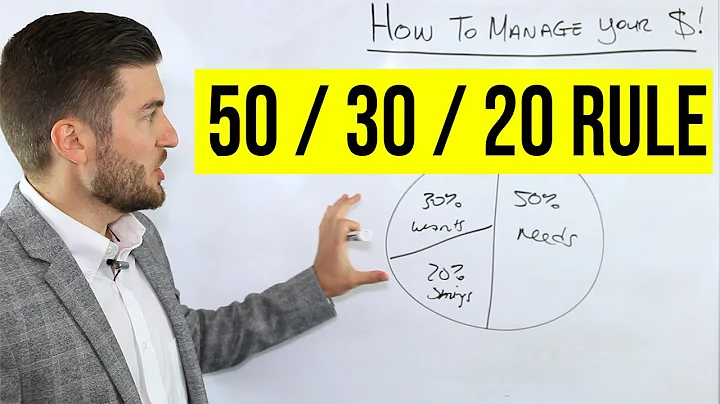

In the next year, you must have a financial management measure that is the most important. It's possible you can do it well, and it's possible you'll make great progress on it. The specific step depends on your own situation. The following factors can help you determine what is most important next year.

1. Make a plan. If you feel that your financial situation is in a mess and you don't know how much savings you have, how much debt you have, and what you have bought, then you'd better get it sorted out starting next year. Figure out your assets and debt situation. Set a goal and then develop a plan to achieve it.

2, credit card bill. If you have been tortured by credit card bills in the past few years, starting from this year, you'd better significantly reduce your credit limit so that you can get out of the debt crisis as soon as possible. If you don't own a home yet, buy one to settle down and start building savings for your children's education and your own retirement.

3, buy a house. If you have a job but don’t own a house yet, you should start saving money for a down payment starting this year. This will definitely sacrifice your quality of life, but if you save money for a year, you can save enough money for the down payment of an ordinary house.

4. Save for college. If you have several children and you don’t have a college fund yet, you should put college funds at the top of your financial list this year. If your children are in high school, now is the time to start saving for college. You can't make enough money in one year to send four children to college for four years (you can't even make enough money in one year to send one child to college for one year, so we have to save for college). However, in one year, you will definitely gain a lot. With such a good start to the year, you can start earning interest on those savings and be good to go.

5, retired. Everyone needs to accumulate for retirement. If your children have left home to study and you are still working, you can start laying the foundation for your retirement life this year. The key to saving for retirement is that the sooner you start, the better. It's much more cost-effective to save a large sum of money as a retirement nest egg a few years before retirement than to save the same amount when you are about to retire.

6, real estate investment plan. If your net worth (total assets minus debts) has accumulated to $1.5 million (congratulations by the way), you need to find a good real estate agent to talk about how to manage your assets and pass them on through reasonable tax avoidance. To your next generation.

7, charity. Of course, you can and should donate some of your money to charity. If you have enough food and clothing in your retirement life, your children have graduated from college, and your investments are in order, you should start doing more charity this year to leave some legacy for future generations and make the world a better place. good.

It’s not just this year, every year there are many new challenges. Make a good plan every year, follow the order of priority, and do everything well. The ultimate goal is to achieve your financial goals and retire the way you want, when you want to retire.